Payday loans are short term, small loans that can be helpful to some people. However, they can also lead to serious problems for borrowers, particularly when they are not repaid on time. This is because payday lenders can charge fees and take collection actions against customers quickly and easily. These types of loans are usually short-term, so the interest rates and fees can make them hard to repay.

There are several ways to avoid this debt cycle. First, you can ask for a payment plan. Most payday loan companies will not agree to do this, but you should still try to find a lender who is willing to work with you. You can also consider taking out a traditional, non-payday loan, if you can afford it.

The other trick is to create a budget. You will have to pay back the loan plus the interest, so you want to make sure you can do it without making a huge dent in your savings. Another option is to start a savings account. Not only will this help you get out of your financial hole, but it will also give you a good idea of how much you can really spend.

You should also seek credit counseling. While you may have trouble finding the money, a nonprofit credit counseling service can give you the tools you need to get out of debt. They can also negotiate a lower repayment plan on your behalf.

Using a website to compare offers from multiple lenders is a good start. Whether you choose a site that has a built in calculator or you have to apply for a loan, it’s a good idea to do a little research to ensure you get the best deal.

You can also check with your state’s attorney general or regulatory agency to see what’s available in your area. Some states have laws in place that regulate fees and interest rates associated with payday loans. Similarly, the District of Columbia outlaws this type of lending.

One of the most important things to learn about these kinds of loans is that they aren’t all that. Some have high interest rates, fees, and other obnoxious requirements. For instance, many will require you to write a post-dated check for the full balance of the loan. If you are unable to pay it off on time, the lender might report you to a credit bureau, resulting in a few high fees.

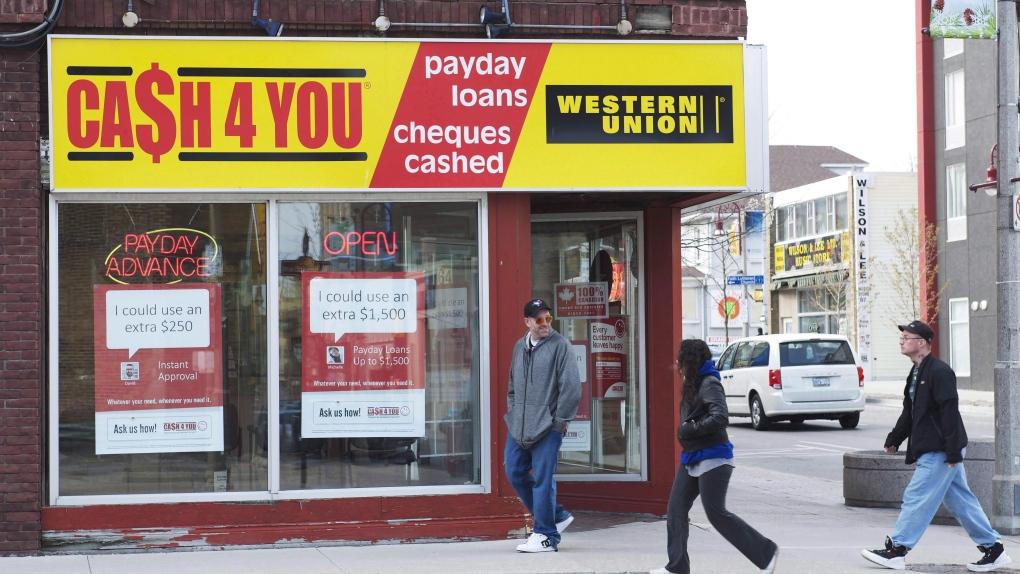

Lastly, you should take a look at Cash 4 You, a Canadian company that isn’t available in your state. Although they have over 100 locations in Ontario, you can only apply for the loan if you are physically able to visit one of their stores.

As a result, Cash 4 You isn’t for everyone. You may be better served by asking a friend or family member for some cash. Alternatively, you can find a less expensive and more flexible personal loan, or even consider a credit union.