Making informed decisions about your finances can be overwhelming, especially when it comes to taking out a personal loan. With so many different loan options available and a vast amount of information online, it can be challenging to know where to start. If you have questions about personal loans, you’re not alone.

In this blog, we’ve compiled a list of frequently asked questions (FAQs) about personal loans in easy-to-understand language. Whether you’re looking to take out a personal loan to consolidate debt or fund a home renovation project, this guide can help you better understand how personal loans work and make more informed borrowing decisions. So, let’s dive in!

1. What is a personal loan and how does it work?

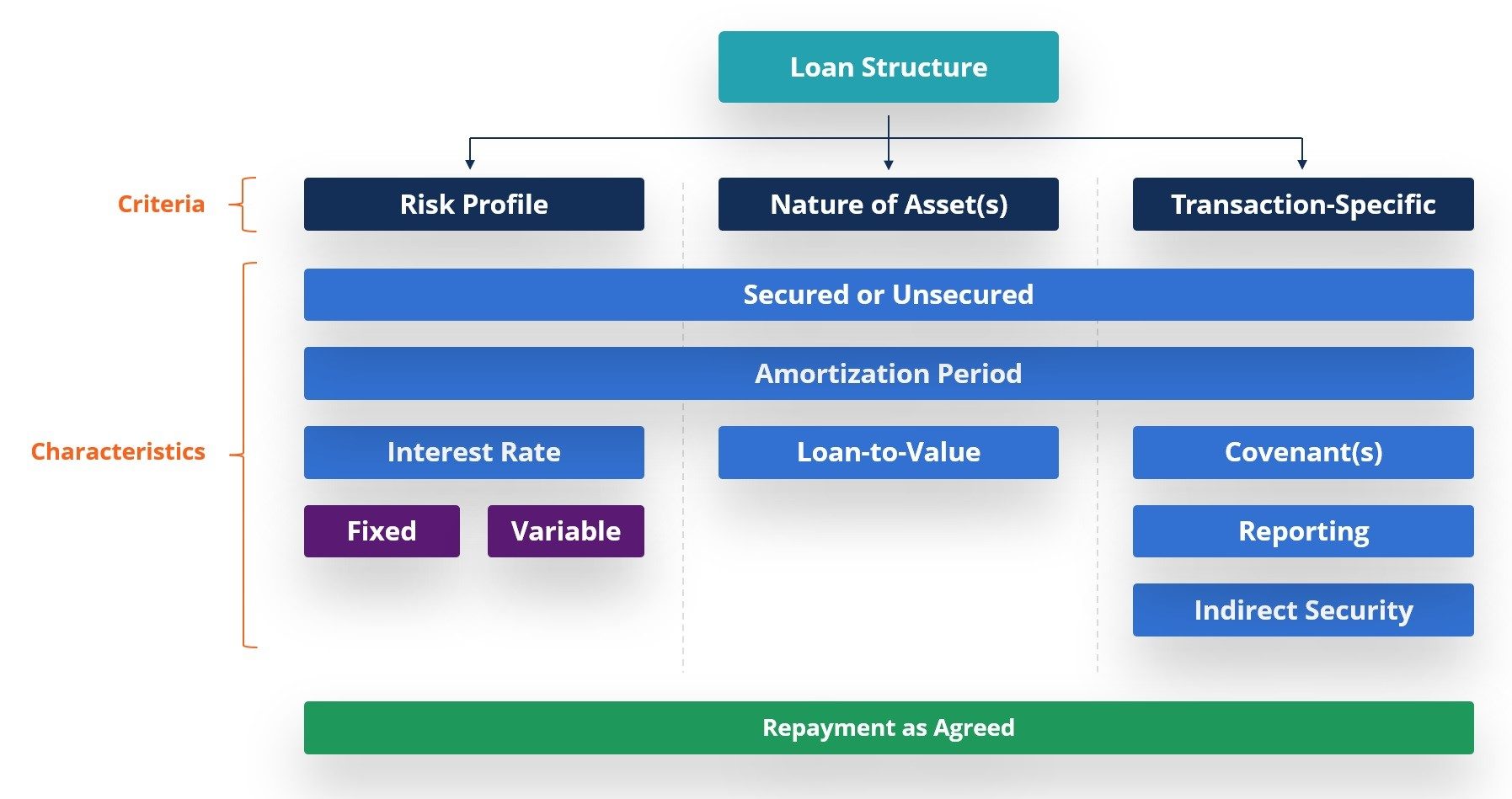

.A personal loan is a type of installment loan that borrowers use to finance a variety of expenses such as home improvements, weddings, or unexpected emergencies. Personal loans are typically unsecured which means that borrowers do not have to put down collateral in order to secure the loan. Instead, lenders will evaluate a borrower’s creditworthiness and income when determining whether or not to approve a loan. Once approved, borrowers receive the loan proceeds as a lump sum and agree to pay it back over a fixed period of time with interest. Repayment terms can vary, but borrowers can typically choose between one and seven years to pay back the loan with equal monthly payments.

2. What are the typical interest rates for personal loans?

Personal loan interest rates can vary based on a variety of factors including the lender, borrower credit score, and loan amount. According to recent data from the Federal Reserve, the average APR on a two-year personal loan is 9.58%, but personal loan rates can currently range from 5.91% to about 35.99%, depending on the lender and borrower creditworthiness. Generally, personal loan companies charge between 7 and 17 percent APR. The interest rate you receive on a personal loan also depends on the term of the loan, with longer loan terms typically resulting in higher interest rates. The good news is that many lenders offer low rates and no fees for personal loans.

:max_bytes(150000):strip_icc()/dotdash-070915-personal-loans-vs-car-loans-how-they-differ-v2-f8faff14abb1488d869f4026c406a86c.jpg)

3. How do I apply for a personal loan?

When it comes to applying for a personal loan, the process may seem overwhelming at first. However, it’s quite simple once you know the steps. First, determine how much you need to borrow and what kind of loan will best suit your needs. Then, gather all the necessary documentation, such as proof of income and identification. Next, shop around for lenders and compare rates and terms. Once you’ve chosen a lender, you can then fill out the application online or in-person. The lender will then review your application and make a decision on whether to approve your loan. If approved, you’ll receive your funds and can start using them for your desired purpose.

4. What is the minimum credit score required for a personal loan?

When applying for a personal loan, one of the most important factors to consider is your credit score. The typical minimum credit score required to qualify for a personal loan is between 560 to 660, according to lenders surveyed by NerdWallet. However, different lenders have different eligibility requirements, so it’s essential to check the minimum credit score required by each lender. For instance, Happy Money requires a FICO score of 640 or higher for approval. Generally, the higher your credit score, the more likely you are to be approved for a personal loan with good rates. However, some lenders offer loans to applicants with lower credit scores.

5. Can I use a personal loan for debt consolidation?

Yes, you can use a personal loan for debt consolidation. Combining multiple loans into one single loan can simplify your financial life and improve your credit. Unsecured personal loans, which don’t require collateral, are often used to consolidate credit card debt. While some lenders offer specialized debt consolidation loans, most standard personal loans can be used for this purpose. It’s important to note that secured loans, such as home and auto loans, cannot be consolidated. Before taking out a personal loan for debt consolidation, it’s important to consider your credit score and any fees associated with the loan. Overall, a personal loan can be a helpful tool for simplifying your debt and improving your financial health.

ankrate.com

ankrate.com6. What is the maximum loan amount I can borrow?

When it comes to personal loans, the maximum loan amount varies depending on the lender and your personal financial situation. Online lenders and banks typically offer loans ranging from $2,000 up to $50,000 or even $100,000 for some borrowers. However, credit unions typically have lower maximum loan amounts, often capping out at $15,000. It’s important to note that just because a lender offers a high maximum loan amount doesn’t mean you will be approved for that amount. Approval depends on factors such as your credit score, income, and debt-to-income ratio. It’s always best to borrow only what you need and can comfortably repay.

:max_bytes(150000):strip_icc()/Term-Definitions_loan.asp-b51fa1e26728403dbe6bddb3ff14ea71.jpg)

7. How long does it take to get approved for a personal loan?

Getting approved for a personal loan differs based on the lender you choose and the information you provide in your application, but generally it takes anywhere from one to ten business days. Some banks can offer approval on the same day as long as you submit all necessary documentation. Online lenders can usually fund loans within one to seven business days after approval. After approval, it may take up to thirty days for loan disbursal. Factors considered in the underwriting process include credit score, income verification, and debt-to-income ratio. With a strong credit score and steady income, the process can be expedited. It’s important to compare rates and fees among lenders and understand the terms before accepting any loan offer.

Source: cdn.corporatefinanceinstitute.com

8. What factors are considered in the underwriting process for a personal loan?

When applying for a personal loan, one of the most important steps is the underwriting process, in which lenders decide whether the applicant is creditworthy and should receive a loan. Lenders consider a variety of factors, including the applicant’s credit score, credit history, current debt-to-income ratio, and collateral. Additionally, lenders may consider the applicant’s income, employment history, and overall financial stability. During the underwriting process, the lender weighs these factors to estimate the chance of default and risk. It’s important for applicants to review all of the requirements, including credit score, income, collateral, and debt-to-income ratio, before applying for a personal loan. With careful consideration and preparation, applicants can increase their chances of approval.

Source: image.cnbcfm.com

9. How long do I have to pay back a personal loan and what are the payment options?

.

When it comes to personal loans, repayment terms can vary greatly depending on the lender and the specific loan agreement. Generally speaking, personal loans typically have repayment terms ranging from one to seven years. The length of your loan will depend on various factors, including the amount you borrow, your income, and your credit history. As for payment options, most lenders will offer a range of options, such as online payments, automatic payments, and even mobile payments. It’s important to choose a payment option that works best for you and fits within your monthly budget. Be sure to read your loan agreement carefully and understand the repayment terms before signing on the dotted line.

10. Are there any additional fees associated with taking out a personal loan?

When considering a personal loan, it’s important to be aware of any additional fees that may come with it. Some lenders may charge a credit check fee or a loan origination fee, which can range from 1% to 10% of the total loan amount. Other fees may include prepayment penalties, which are fees charged if you pay off the loan early. However, not all lenders charge these fees. For example, DCU offers personal loans with no loan origination fee. It’s important to do your research and compare different lenders to find the best option that fits your financial needs.

4. What is the minimum credit score required for a personal loan?

When applying for a personal loan, one of the most important factors to consider is your credit score. The typical minimum credit score required to qualify for a personal loan is between 560 to 660, according to lenders surveyed by NerdWallet. However, different lenders have different eligibility requirements, so it’s essential to check the minimum credit score required by each lender. For instance, Happy Money requires a FICO score of 640 or higher for approval. Generally, the higher your credit score, the more likely you are to be approved for a personal loan with good rates. However, some lenders offer loans to applicants with lower credit scores.

5. Can I use a personal loan for debt consolidation?

Yes, you can use a personal loan for debt consolidation. Combining multiple loans into one single loan can simplify your financial life and improve your credit. Unsecured personal loans, which don’t require collateral, are often used to consolidate credit card debt. While some lenders offer specialized debt consolidation loans, most standard personal loans can be used for this purpose. It’s important to note that secured loans, such as home and auto loans, cannot be consolidated. Before taking out a personal loan for debt consolidation, it’s important to consider your credit score and any fees associated with the loan. Overall, a personal loan can be a helpful tool for simplifying your debt and improving your financial health.

6. What is the maximum loan amount I can borrow?

When it comes to personal loans, the maximum loan amount varies depending on the lender and your personal financial situation. Online lenders and banks typically offer loans ranging from $2,000 up to $50,000 or even $100,000 for some borrowers. However, credit unions typically have lower maximum loan amounts, often capping out at $15,000. It’s important to note that just because a lender offers a high maximum loan amount doesn’t mean you will be approved for that amount. Approval depends on factors such as your credit score, income, and debt-to-income ratio. It’s always best to borrow only what you need and can comfortably repay.

7. How long does it take to get approved for a personal loan?

Getting approved for a personal loan differs based on the lender you choose and the information you provide in your application, but generally it takes anywhere from one to ten business days. Some banks can offer approval on the same day as long as you submit all necessary documentation. Online lenders can usually fund loans within one to seven business days after approval. After approval, it may take up to thirty days for loan disbursal. Factors considered in the underwriting process include credit score, income verification, and debt-to-income ratio. With a strong credit score and steady income, the process can be expedited. It’s important to compare rates and fees among lenders and understand the terms before accepting any loan offer.

8. What factors are considered in the underwriting process for a personal loan?

When applying for a personal loan, one of the most important steps is the underwriting process, in which lenders decide whether the applicant is creditworthy and should receive a loan. Lenders consider a variety of factors, including the applicant’s credit score, credit history, current debt-to-income ratio, and collateral. Additionally, lenders may consider the applicant’s income, employment history, and overall financial stability. During the underwriting process, the lender weighs these factors to estimate the chance of default and risk. It’s important for applicants to review all of the requirements, including credit score, income, collateral, and debt-to-income ratio, before applying for a personal loan. With careful consideration and preparation, applicants can increase their chances of approval.

9. How long do I have to pay back a personal loan and what are the payment options?

.

When it comes to personal loans, repayment terms can vary greatly depending on the lender and the specific loan agreement. Generally speaking, personal loans typically have repayment terms ranging from one to seven years. The length of your loan will depend on various factors, including the amount you borrow, your income, and your credit history. As for payment options, most lenders will offer a range of options, such as online payments, automatic payments, and even mobile payments. It’s important to choose a payment option that works best for you and fits within your monthly budget. Be sure to read your loan agreement carefully and understand the repayment terms before signing on the dotted line.

10. Are there any additional fees associated with taking out a personal loan?

When considering a personal loan, it’s important to be aware of any additional fees that may come with it. Some lenders may charge a credit check fee or a loan origination fee, which can range from 1% to 10% of the total loan amount.

Other fees may include prepayment penalties, which are fees charged if you pay off the loan early. However, not all lenders charge these fees.

For example, DCU offers personal loans with no loan origination fee. It’s important to do your research and compare different lenders to find the best option that fits your financial needs.